How East Bay Sellers Are Using Bridge Loans to Move Up, Move Out, and Win Offers

One of the most stressful parts of selling a home is figuring out what comes next. You need to sell, but you also need somewhere to live. And if you want to buy in a market like Danville or Concord, showing up with a contingent offer tied to your current sale puts you at an immediate disadvantage.

This article breaks down the three main paths East Bay homeowners take: sell first and buy after, try to do both simultaneously, or use a bridge loan to buy first and sell with leverage. We cover how each strategy works, where bridge financing makes the most sense in our market, and the real costs and risks you need to understand before you commit.

The East Bay Market in 2026: Where Sellers Stand

Before deciding on a strategy, you need to understand what the market is doing in your specific city. The East Bay is not one market. Danville and Concord are performing very differently from Pinole and Hercules right now.

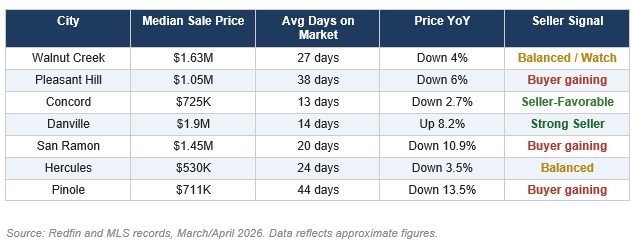

Here is a snapshot of current conditions across the cities we serve, based on Redfin and MLS data through early 2026.

What This Means for Sellers

Danville remains the strongest seller's market in this group. Prices are up 8.2% year-over-year, homes move in roughly 14 days, and buyer demand for the school district and lifestyle continues to hold. If you are selling here, you have pricing power.

Concord is punching above its price point. With 56% of homes selling above asking and a sale-to-list ratio above 101%, this is one of the most active seller markets in Contra Costa County right now. The entry-level price point is driving strong demand.

Walnut Creek shows a slight softening with prices down about 4% year-over-year and days on market ticking up. It is not a buyer's market, but sellers need to price accurately.

Pleasant Hill and San Ramon are showing more buyer influence. Prices are down, and both markets are taking longer to move inventory than a year ago.

Hercules and Pinole are facing headwinds. Pinole is down 13.5% year-over-year, and days on market in both cities have stretched. Sellers here need realistic pricing and, if moving up, should think carefully about timing and offer strategy.

Three Ways to Navigate the Buy-Sell Transition

There is no single right answer. Each approach involves tradeoffs based on your equity, timeline, financial position, and how competitive the market is where you are buying.

Option 1: Sell First, Then Buy

You list your home, accept an offer, close, and then go find your next property. You know exactly how much you netted. You shop with a clean balance sheet. Offers you make are not contingent on your sale, which strengthens your position.

The downside is practical: you need somewhere to live between closings. That usually means temporary housing, a rent-back agreement with your buyer, or staying with family. In a fast-moving market, you may also feel pressure to buy quickly and end up settling.

This strategy works best when the city you are moving to has reasonable inventory and you have flexibility on timing.

Option 2: Buy and Sell Simultaneously

You try to coordinate both transactions to close around the same time. You make your purchase offer contingent on the sale of your current home.

In theory this is clean. In practice it is the hardest to execute. Sellers in strong markets like Danville and Concord are often unwilling to accept contingent offers when non-contingent buyers are in the mix. You may lose multiple homes before landing one. And if your sale falls through, your purchase is at risk too.

This approach is more viable in softer markets where sellers have fewer options. If you are buying in Hercules or Pinole while also selling there, it may be workable.

Option 3: Bridge Loan

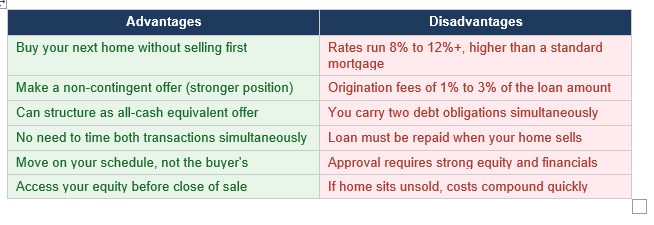

A bridge loan lets you tap the equity in your current home before it sells. You use those funds for the down payment and closing costs on your next home. Then, once your current home sells, you pay off the bridge loan.

This removes the contingency from your offer. You can compete on equal footing with other buyers, and in some cases structure your offer to present as cash, which is a significant competitive advantage in markets like Danville where multiple offers are common.

How a Bridge Loan Works

The basic structure is straightforward. Lenders will typically lend up to 80% of your current home's appraised value, minus your existing mortgage balance.

Example: Your home is worth $900,000. You owe $350,000 on it.

($900,000 x 0.80) minus $350,000 = $370,000 available through the bridge loan.

You use that $370,000 as a down payment on your next home, close on the purchase, then sell your current home and pay off the bridge.

Bridge loans are short-term, typically 6 to 18 months. They are interest-only, meaning you are not paying down principal during the loan term. The balloon balance is due when your current home closes.

Current Bridge Loan Costs (2026)

• Interest rates: 8% to 12% depending on lender, property, and borrower profile

• Origination fees: 1% to 3% of the loan amount

• Loan term: typically 6 to 18 months

• Approval timeline: significantly faster than a conventional mortgage, often 10 to 20 days

On a $370,000 bridge loan at 9%, your monthly interest-only payment would be approximately $2,775. Over six months, that is about $16,650 in interest before fees. That is the cost of moving without waiting.

Advantages and Disadvantages: The Full Picture

When Bridge Loans Make the Most Sense

Bridge financing is most valuable in competitive markets where contingent offers get passed over. In the East Bay right now, that points primarily to:

• Danville: active demand, fast-moving inventory, sellers routinely receiving multiple offers

• Concord: over 56% of homes selling above asking, extremely low days on market

• Walnut Creek: well-priced homes still moving quickly, non-contingent offers command attention

If you are in Pinole or Hercules, where the market is slower, a bridge loan may be less necessary. You have more time to coordinate, and sellers in those markets are generally more receptive to contingent buyers.

Positioning as an All-Cash Buyer

The most powerful version of a bridge loan strategy is combining it with a cash offer program. Several lenders and real estate platforms will use your bridge loan proceeds to make an actual all-cash offer on your behalf. You then get conventional financing once you close.

In markets like Danville where luxury buyers are common and sellers want certainty, presenting as a cash buyer can move you to the top of the pile even if you are not technically paying cash out of pocket.

How to Structure This

• Work with a lender experienced in bridge financing, not just a standard bank

• Get your current home appraised and understand your available equity before you start shopping

• Have your bridge loan pre-approved so you can move fast when the right home appears

• Confirm your exit strategy: your current home should be priced to sell within the bridge loan term

• Model the carrying costs: interest plus fees plus temporary housing if applicable, and make sure the numbers work

The Risk You Cannot Ignore

Bridge loans are a powerful tool, but they amplify risk when things do not go to plan. If your current home takes longer to sell than expected, you are carrying two sets of payments. If you overprice your current home to net more, you may extend the timeline and burn more in bridge loan interest than you gained.

In a market like Pinole, where days on market have climbed to 44 and prices are down over 13% year-over-year, a seller counting on a fast exit to pay off a bridge loan needs to be realistic about pricing from the start.

The bridge loan works when you go into it with a well-priced home, a clear timeline, and a lender who has given you a realistic term. It does not work as a way to avoid a price reduction while hoping the market turns.

The Bottom Line

For most East Bay homeowners who have built up equity and need to move, the bridge loan path offers real advantages. You stop being a contingent buyer, you can move on your schedule, and in the right market you can structure an offer that looks like cash.

The cost is real: interest rates are high relative to conventional mortgages, and fees add up. But when weighed against the cost of missing out on a home or losing a bidding war because of a contingency, many sellers find the math works.

Whether this is the right move for you depends on your equity position, your financial cushion, and which city you are selling in. Markets like Danville and Concord favor sellers who can show up ready to close. Markets like Hercules and Pinole give you more time and more negotiating room with buyers.

Start by knowing your numbers. Know your current home's value, your equity, and what a bridge loan would cost you over the likely selling timeline. From there, you can make a clear-eyed decision.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or tax advice. Market data referenced is sourced from Redfin and MLS records as of March/April 2026 and is subject to change. Consult a licensed broker, financial advisor, and lender before making any real estate or financing decisions.

Parm Rahi is a licensed real estate broker. East Bay Home Sellers is a publication covering residential real estate across Contra Costa Coun